The Congressional Budget Office (CBO) released, on March 30, its analysis of the President’s Fiscal Year (FY) 2021 budget using its own assumptions to evaluate the budget’s policies. Importantly, all of these estimates exclude the fiscal and economic effects of the novel coronavirus (COVID-19) outbreak and efforts to mitigate it.

CBO’s estimates show that debt and deficits under the President’s budget would rise over the next decade, rather than fall as the White House claims.

In this paper, we show:

-

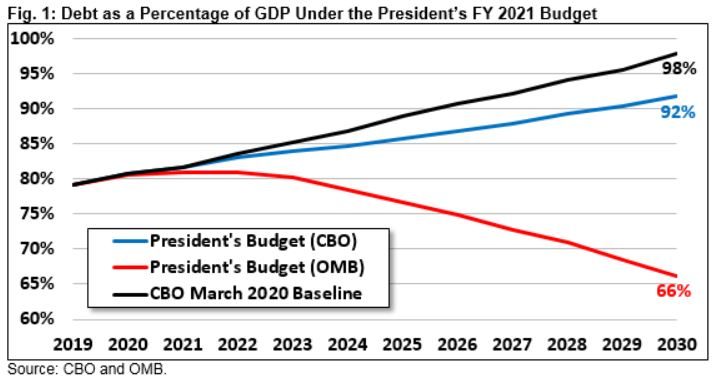

Debt under the President’s budget would rise from over 80 percent of Gross Domestic Product (GDP) today to almost 92 percent by 2030, rather than falling to 66 percent of GDP as the Office of Management and Budget (OMB) projects.

-

Deficits under the President’s budget would total $11 trillion over the next decade, rising from $984 billion last year to $1.4 trillion by 2030. By comparison, OMB estimated deficits would total $5.6 trillion over a decade and fall to $261 billion by 2030.

-

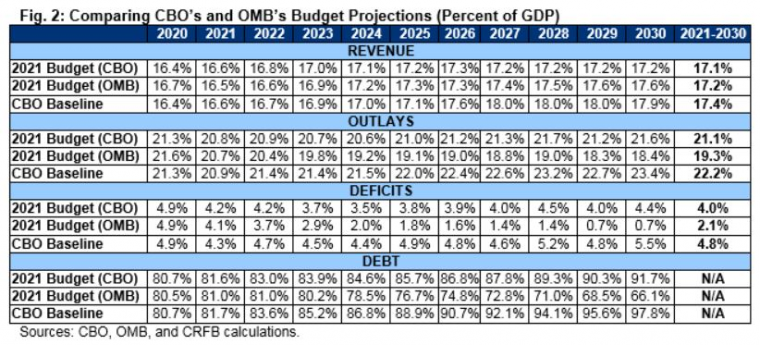

CBO estimates revenue would average 17.1 percent of GDP under the President’s budget, similar to OMB’s estimated 17.2 percent. CBO estimates spending would average 21.1 percent of GDP, compared to OMB’s 19.3 percent.

-

In total, CBO estimates the President’s budget would reduce deficits by $2.1 trillion over a decade — the net effect of a $2.8 trillion reduction in spending, a $936 billion reduction in revenue, and $237 billion in interest savings. The largest spending cuts come from lower nondefense discretionary spending and reductions in health-care costs. Much of the reduction in revenues comes from the extension of individual income and estate tax provisions in the 2017 tax law.

-

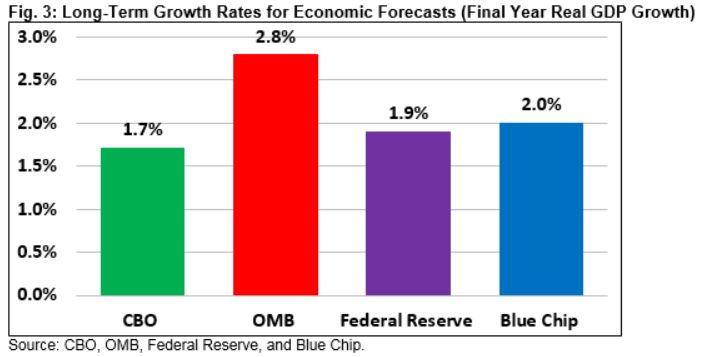

The disconnect between CBO’s and OMB’s estimates is largely driven by different economic assumptions. While CBO’s economic estimates mirror those of other forecasters, OMB relies on overly-optimistic economic-growth assumptions. CBO estimates (pre-COVID-19) real GDP growth will average 1.7 percent over the next decade, while OMB assumes an average of 2.9 percent.

While policymakers must focus all of their attention on the current economic and public health crisis, at some point they will need to turn their efforts to taming what will be a much higher federal debt. The President’s budget offers a number of thoughtful proposals to reduce health care costs and spend more efficiently. Unfortunately, it falls short of what is claimed and well short of what is needed to stabilize the national debt, let alone reduce it to more sustainable levels.

Debt, Deficits, Revenue, and Spending in the President’s Budget

CBO finds that debt under the President’s budget would rise over the next decade, from over 79 percent of GDP in 2019 to 83 percent in 2022 and 92 percent of GDP by 2030. While this is somewhat lower than the 98 percent of GDP in 2030 projected under current law, it is significantly higher than OMB’s projection, which estimates debt would peak at 81 percent of GDP in 2022 before declining to 66 percent of GDP by 2030.

CBO finds that annual deficits under the President’s budget would decline from $1.1 trillion in 2020 to $900 billion in 2024 before rising to $1.4 trillion in 2030. As a share of the economy, CBO expects deficits under the President’s budget would decline from 4.9 percent in 2020 to 3.5 percent by 2024 before rising to 4.4 percent of GDP by 2030. CBO’s projection for the 2030 deficit is somewhat below its current law estimate of $1.8 trillion (5.5 percent of GDP) but much higher than OMB’s $261 billion (0.7 percent of GDP) estimate.

Revenue under the President’s budget would rise gradually from 16.3 percent of GDP in 2019 to 17.2 percent of GDP by 2025, remaining at roughly that level for the rest of the decade. Spending, meanwhile, would shrink slightly to 20.6 percent of GDP by 2024 before rising once again, reaching 21.6 percent of GDP by 2030. Both revenue and spending would be lower in 2030 than under current law (17.9 and 23.4 percent of GDP, respectively). They would also differ significantly from OMB’s estimates that revenue would reach 17.6 percent of GDP and spending would reach 18.4 percent by 2030.

CBO finds that deficits would total $11 trillion (4 percent of GDP) between 2021 and 2030 under the President’s budget, which is $5.4 trillion higher than OMB’s projection but $2.1 trillion lower than current law.

The $2.1 trillion of deficit reduction from the President’s budget is the net effect of $3 trillion less in spending and over $900 billion less in revenue. A complete summary of the proposals in the President’s budget can be found here.

Spending reductions include $2.1 trillion from discretionary programs, nearly $600 billion from lower federal spending on health care, about $80 billion in further net spending reductions (a combination of cuts and increases), and more than $200 billion less in net interest spending.

Revenue reductions largely result from extending large parts of the Tax Cuts and Jobs Act beyond 2025 — which would be responsible for about $1.2 trillion in lost revenue. New tax credits for scholarship donations would lose another $50 billion of revenue. Other revenue measures, including stronger IRS tax enforcement, repeal of energy tax credits, and increased federal employee retirement contributions, would offset this reduction by raising almost $300 billion.

The Committee for a Responsible Federal Budget will publish a more complete analysis of the fiscal impact of policies in the President’s budget in the coming days.

Differences Between CBO’s and OMB’s Estimates

CBO estimates debt and deficits would be much higher under the President’s budget than OMB projects. CBO expects deficits would total $11.0 trillion over the next decade, which is $5.4 trillion higher than OMB’s estimate of $5.6 trillion. At the same time, debt in 2030 under CBO’s estimate would be much higher: 92 percent of GDP instead of 66 percent.

The bulk of the disconnect between CBO’s and OMB’s estimates stems from different economic assumptions. CBO projects real economic growth will average 1.7 percent over the next decade, which was in line with the projections of other forecasters prior to the COVID-19 outbreak. Meanwhile, OMB projects that real GDP will grow by an average of 2.9 percent, a projection far outside mainstream forecasts and which was highly unlikely to materialize on a sustained basis even before the current crisis. In reality, the economy is likely to contract in 2020, and long-term growth is highly uncertain but doubtful to approach the Administration’s estimates for any sustained period.

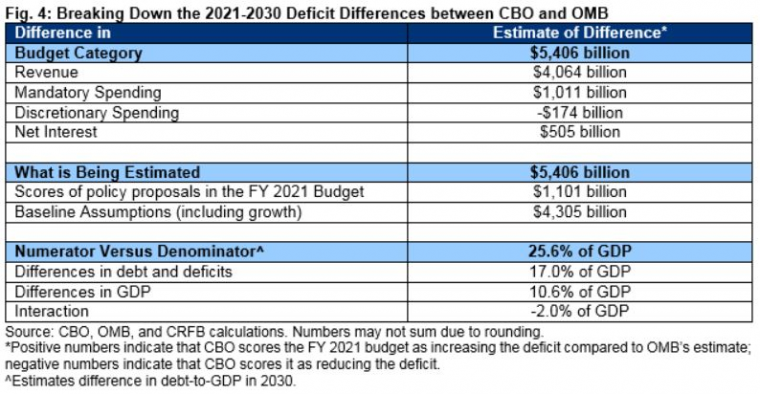

CBO’s more reasonable economic growth assumptions lead to a projection of $4.1 trillion less in revenue over a decade than OMB does, accounting for the bulk of the $5.4 trillion difference in projected deficits between the two estimators. CBO also projects primary spending would be more than $800 billion higher than OMB and interest costs would be more than $500 billion higher.

Both on the revenue and spending side, the vast majority of the difference between CBO and OMB is due to the economics in the underlying baseline projections. While CBO believes the President’s policies would save about $1.1 trillion less than OMB forecasts, it also projects that baseline deficits will be about $4.3 trillion higher.

It is worth noting that focusing only on the $5.4 trillion difference in deficit projections understates the difference between CBO’s and OMB’s estimates since it focuses on nominal deficits rather than debt as a share of GDP. In total, debt-to-GDP is projected to be about 26 percentage points higher under CBO’s estimate. About three-fifths of the difference stems from higher projected debt levels, while the remaining two-fifths is attributable to lower GDP estimates.

Some of the difference between CBO’s and OMB’s estimates may be due to the fact that the latter — by convention — incorporates the impact of the President’s budget into its analysis while CBO does not. However, any reasonable estimate of dynamic feedback from the President’s budget would be modest compared to the overall difference in economic growth rates.

Conclusion

CBO’s analysis shows that with realistic economic assumptions, debt under the President’s budget would rise as a share of the economy, not fall as the White House claims, and trillion-dollar annual deficits would only briefly disappear before returning indefinitely. Incorporating the effects of the COVID-19 outbreak on the economy and budget, debt will inevitably grow far higher. Nevertheless, the debt trajectory under the President’s budget would be an improvement over current law.

The President deserves credit for setting the goal of reducing debt as a share of GDP and putting forward a number of thoughtful policies to achieve that goal. Unfortunately, the budget relies on overly optimistic economic assumptions, unrealistic or unspecific policy assumptions, and other gimmicks to make the fiscal outlook seem brighter than it actually is.

As the U.S faces a sudden economic downturn in the wake of the COVID-19 pandemic, deficit reduction will not and should not be the primary focus of elected officials. But when we get through this crisis, reasonable and thoughtful approaches to reduce the national debt will be needed more than ever. Many of the policies in the President’s budget would represent a good starting point for addressing structural deficits and putting debt and deficits on a sustainable long-term path. However, more significant revenue increases and spending reductions will be needed.