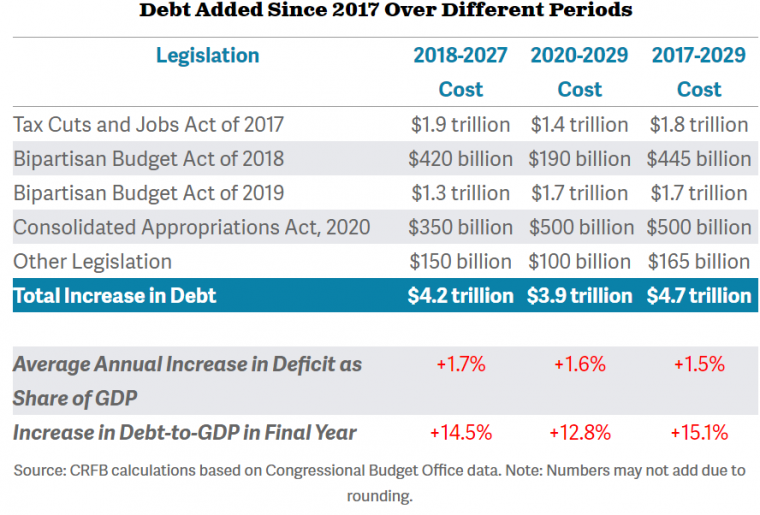

WASHINGTON DC (January 10, 2020) — Last summer, we estimated that since his inauguration in January of 2017, President Trump had signed legislation into law that will ultimately add $4.1 trillion to the national debt from 2017 to 2029. After the December appropriations bills — which were first passed by a Democratic House and a Republican Senate before being signed by the President — we now estimate he has signed legislation adding $4.7 trillion to the national debt between 2017 and 2029. Over a ten-year budget window that is traditionally used to evaluate legislation, the President will have added $3.9 to $4.2 trillion to the debt, depending on the window. The source of the debt increase is split relatively evenly between tax and spending policy changes.

The Tax Cuts and Jobs Act (TCJA) alone added a projected $1.8 trillion to the debt, including interest and dynamic effects, through 2029. Even this number assumes that the individual tax cuts under the law expire as scheduled after 2025. An additional $1 trillion could be added to the debt through 2029 if the individual tax cuts are extended.

The Bipartisan Budget Act (BBA) of 2018 and Bipartisan Budget Act of 2019 added a combined $2.2 trillion to projected debt, mainly by dramatically increasing defense and non-defense spending caps for 2017 through 2021. Since no budget caps exist after 2021, CBO assumes spending will continue to grow with inflation after 2021, so the bills will increase spending by similar amounts in future years.

Finally, the December 2019 spending deal added $500 billion of debt by tacking onto ordinary appropriations a number of tax cuts. Most significantly, the bill permanently repealed three taxes meant to fund the Affordable Care Act, including the Cadillac tax that economists agree would have slowed health care cost growth and significantly reduced deficits over the long term. The legislation also revived a series of temporary special-interest zombie tax breaks, most of which had been expired for two years.

Other pieces of legislation account for nearly $165 billion of debt. This includes several different bills containing disaster relief and emergency spending as well as continued delaysof the three ACA taxes that were subsequently repealed in December’s spending package deal, among other small items.

Importantly, this analysis does not account for any regulatory changes and covers a 13-year period from 2017 to 2029 (though nearly all costs are from 2018-2029). Using a standard ten-year budget window, we estimate President Trump signed $4.2 trillion of debt increases into law between 2018 and 2027, or $3.9 trillion from 2020 to 2029. The slightly lower cost in the later window is driven by the individual tax cut expirations after 2025 (see above graphic).

The $4.7 trillion of debt signed into law by President Trump is on top of the current $17.2 trillion debt held by the public and the $9.2 trillion we were already expected to borrow over the next decade absent these proposals. Debt is projected to be about 97 percent of Gross Domestic Product (GDP) in 2029, compared to 82 percent if none of this debt-increasing legislation had been passed.

It is worth keeping in mind that Congress — not the President — is primarily responsible for setting the federal budget and shaping federal tax and spending policy. There is little the President can do to impact the debt, positively or negatively, without a bill passed by Congress. Conversely there is little Congress can do without the President's signature or a veto-proof supermajority. Furthermore, control of Congress has been split between a Democratic House and a Republican Senate for the past year — one-third of Trump’s presidency thus far. In reality, both the executive and legislative branches of the federal government share blame, not just for passing new legislation that adds to the debt, but also for failing to address existing problems like the growing cost of entitlement programs or insufficient revenues that have added to the debt for years.

Debt is rising on an unsustainable path. Thanks to legislation passed since 2017, the nation is facing trillion-dollar annual deficits for the foreseeable future and without action is almost certain to surpass the record debt levels set after World War II in the coming years. As we begin 2020, lawmakers should make a new year’s resolution to consider budget offsets for any new spending or tax cut proposals, reform the TCJA from a budget-buster into a pro-growth tax reform, and make sure our nation’s health and retirement programs are adequately funded for future generations.